Kvants.ai is a #AI Powered Asset Management Platform Bringing Automated Quantitative Strategies to Everyday Investors.

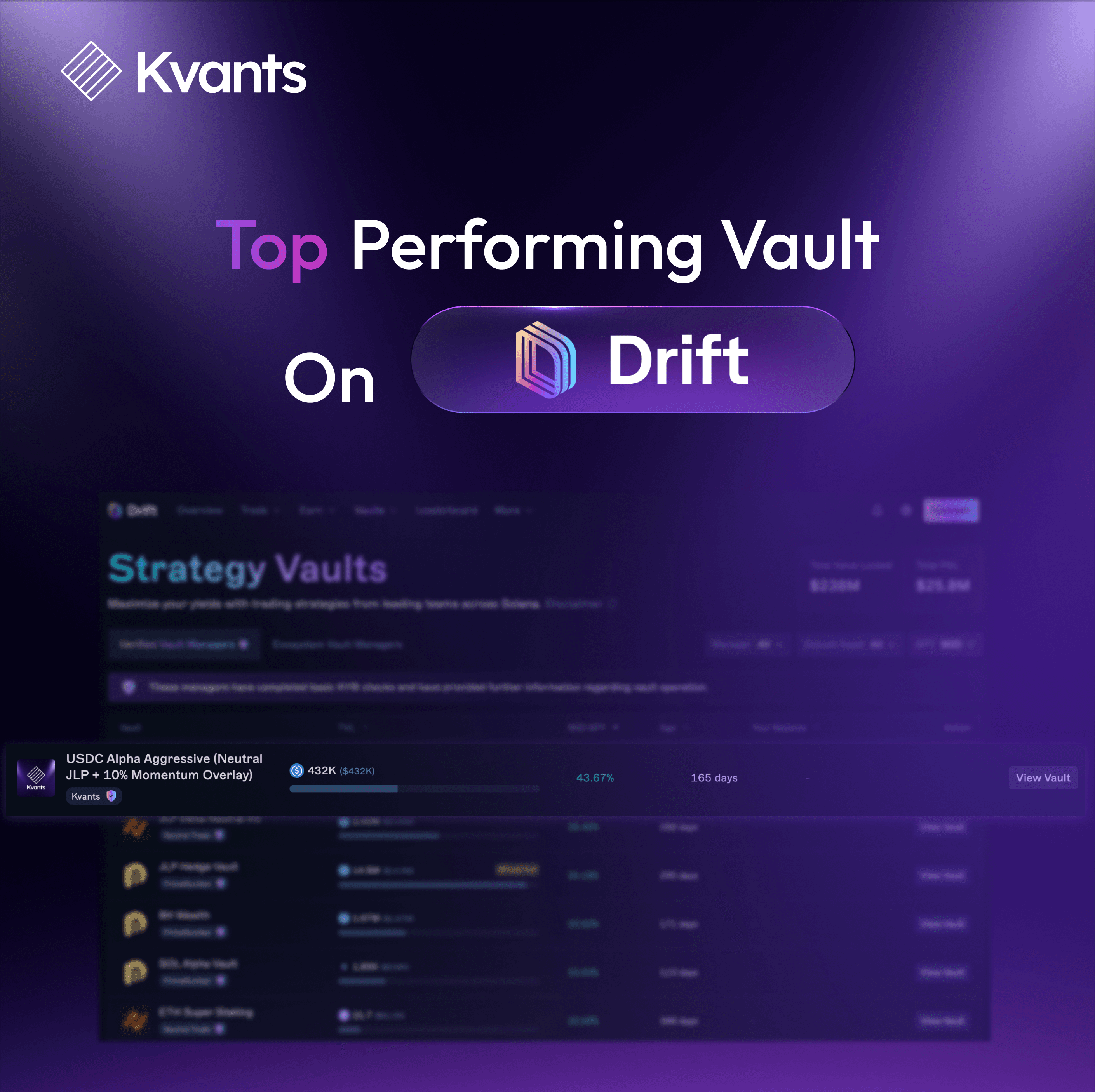

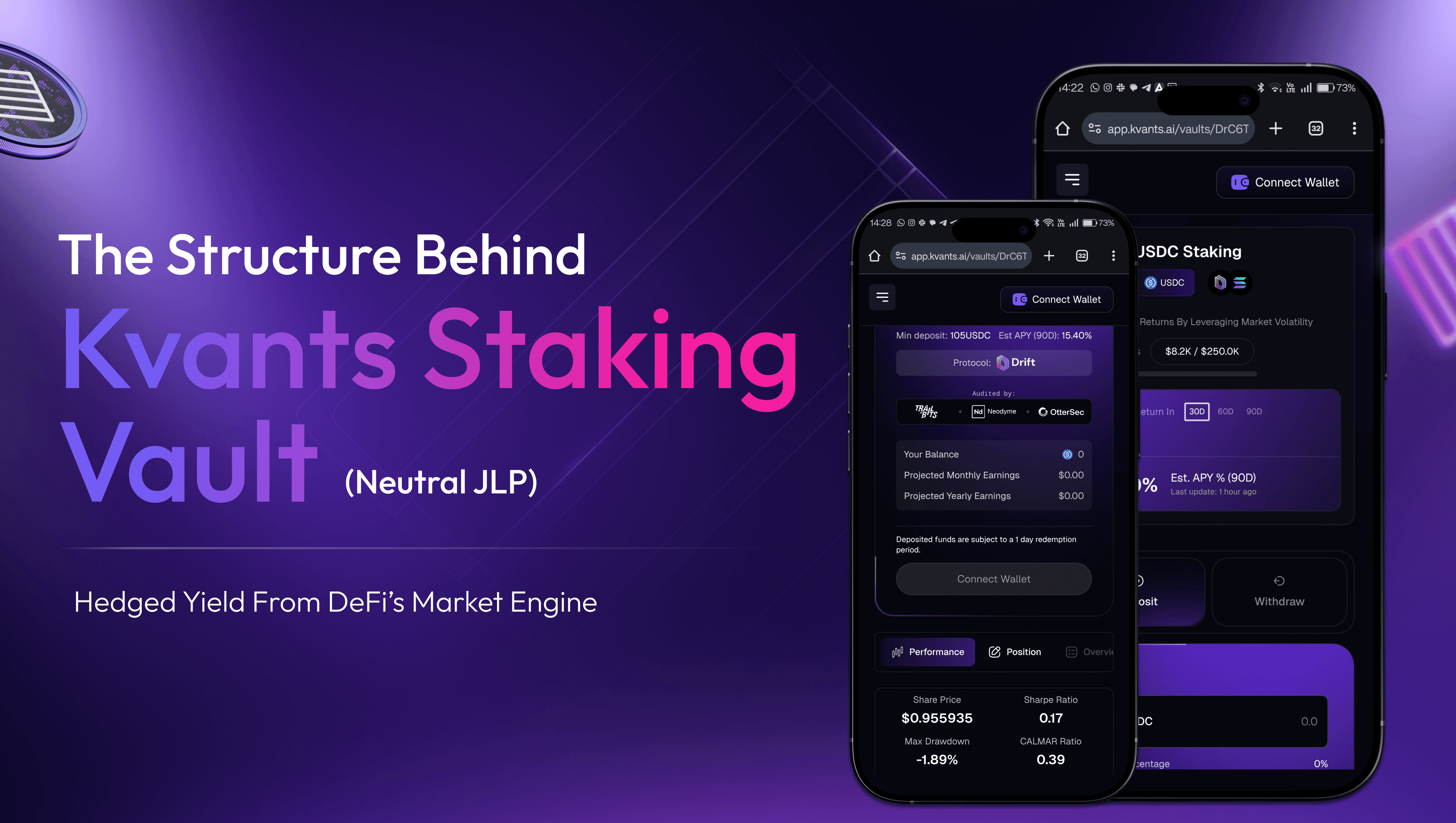

Apr 7 | 3 Minutes MIN | Drift Vaults

Feb 9 | 5 Minutes MIN | Kvants, AI, DeFi, TGE, Token Launch

Jan 25 | 5 Minutes MIN | AI, DeFi

Jan 6 | 7 Minutes MIN | Kvants

Jan 6 | 5 Minute MIN | Year In Review, Updates

Dec 19 | 5 Mins MIN | Product

Dec 2 | 5 mins MIN | Product

Nov 27 | 5 mins MIN | Product

Nov 25 | 5 mins MIN | Product

Nov 21 | 5 Mins MIN | Product

Nov 13 | 5 Mins MIN | Product

Nov 12 | 5 Mins MIN | Product